Nudging the Self-Employed into Contributing to Social Security

Context

Understanding how to successfully promote retirement savings and social security contributions is crucial for economic development and stability. In Latin America and the Caribbean, public spending on social security as a percentage of GDP averaged 3.3 percent in 2015 and is predicted to reach 18 percent by 2100 despite rampant evasion and underreporting. Half of salaried workers contribute to social security, but only 16 percent of the self-employed do. As a result, by 2050 47 to 60 percent of elderly adults will lack necessary savings (or pension eligibility) to sustain themselves upon reaching retirement age. The region faces the challenge of providing adequate income to the 140 million expected retirees; using behavioral economics tools such as reminders, defaults, and commitments can facilitate this endeavor.

The Project

In 2009, Brazil’s Ministry of Social Security launched a program aimed at reducing the burden of social security and tax on independent micro entrepreneurs (MEI) from 20 to 7 percent of their average net income, while increasing compliance rates. It also simplified payment by combining municipal and state levies. Yet, two years into the program, only 2 million of Brazil’s 9 million self-employed workers had enrolled in it. Of those, only 45 percent made regular payments. Moreover, in a survey conducted in 2013 by the program administrator, 20 percent of the affiliates responded that they were not aware that registration in the MEI required their monthly contributions.

To increase contributions from the self-employed, Brazil’s Ministry of Social Security and the IDB mailed a booklet to 3 million self-employed workers, reminding them of their obligation and highlighting the benefits of contributing to social security.

In order to pay for the contributions, all MEI beneficiaries had to go online and either make the payment through the online banking system or print a voucher (boleto bancário), a Brazilian print-payment instruction accepted by all banks.

Behavioral Analysis

Behavioral Barriers

Present bias: It is the tendency to choose a smaller gain in the present over a large gain in the future. It is related to the preference for immediate gratification. It is also known as hyperbolic discounting. People with such a bias might value present gratification more than greater benefits in the future—for example, they might prefer to spend time and money on the present instead of saving for their future self.

Hassle factors: Seemingly small inconveniences, such as having to read a lot of information or take an extra small step to complete an action, can hinder or disrupt decision-making processes. For example, self-employed workers may have a hard time accessing their banking system or printing a voucher.

Cognitive overload: The cognitive load is the amount of mental effort and memory used at a given moment in time. ‘Overload’ occurs when the volume of information presented exceeds an individual’s capacity to process it. Thus, the fact that our attention and memory are limited prevents us from processing all available information at the same time. This leads, for example, to forgetting to pay bills.

Status quo (inertia): It is the tendency to maintain the current state of affairs, even when change is clearly better. This current status, or status quo, is used as a reference point, and any change with regard to this reference is seen as a loss. For example, the current status for the self-employed is not to contribute to social security, so deviating from this status is hard.

Behavioral Tools

Reminders: They can take many forms, such as an email, a text message, a letter, or an in-person visit reminding individuals of some aspect of their decision-making process. Reminders are designed to mitigate procrastination, oversight, and cognitive overload.

Prominence: Human beings have limited stores of attention. Making key elements visible and prominent at the proper time and place is as important as the message itself.

Planning tools: These are designed to encourage individuals to make a concrete action plan on important goals, like paying social security. These prompts help individuals to break down a goal (e.g., being on time to a doctor’s appointment) into a series of small, specific tasks (e.g., leaving work early, finding a babysitter, postponing a weekly meeting, etc.) and to anticipate unforeseen events. These prompts often encourage people to write down relevant information such as the date, time, and place of a commitment.

Simplification: Reducing the effort required to perform an action. For example, cutting the number of steps involved in achieving a complex goal, or break it down into simpler steps.

Intervention Design

The MEI booklet explains social security thus: “Keeping up with the monthly payments, you are protected in case of an accident, entitled to an old-age pension, a disability pension, maternity leave (in case of pregnant women and adoptions) after a minimum number of contributions. Your family will have the right-of-survivorship pension and pension-grant.”

The booklet can be understood as a composite of several behavioral interventions: First, it acts as a reminder, drawing attention to the issue and highlighting information related to compliance with social security and tax authorities. Second, it highlights the importance of the contribution to become eligible for a series of benefits.

Additionally, it can be perceived as a monitoring tool, as it bears both the seal of the Ministry of Finance (Ministerio da Fazenda) and the Ministry of Social Security to reinforce the urgency of the matter. Finally, it also offers simplification and a planning tool, as it contains 12 blank vouchers (boletos bancários) for a year’s monthly installments.

The intervention staggered implementation over a four-month period across four states, resulted in a quasi-natural experiment involving 3 million self-employed workers across 5,396

Results

Reminders appear to have a significant impact on savings decisions and to have dramatically increased savings for retirement.

- Sending the booklet increased social security payments by 15 percent and tax compliance rates by 7 percentage points (from 40 to 47 percent).

- Workers affiliated with social security increased contributions markedly the month they received the booklet, although these immediate gains decreased rapidly, disappearing after three months.

- The relatively brief increase in payments over a period of six months outweighs the cost of sending the booklet by at least a factor of two, increasing social security contributions (net of costs) by $3.1 million.

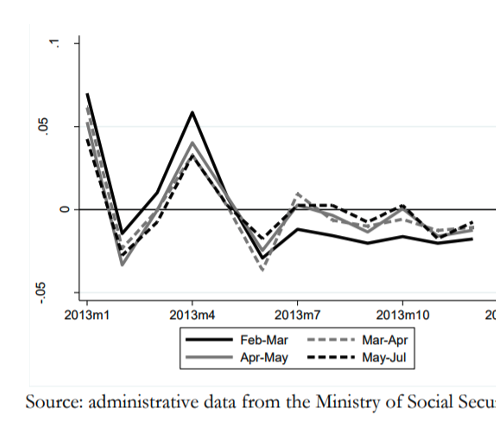

Figure 1. Trends in Pretreatment Compliance Rates (2013)

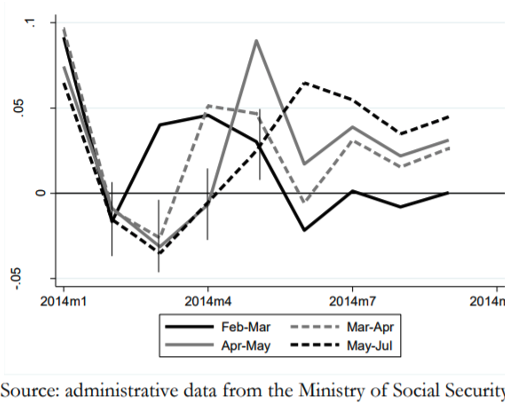

Figure 2. Trends in Posttreatment Compliance Rates (2014)

Policy Implications

- Behavioral tools, such as reminders, can have a significant impact on financial decisions and dramatically increase savings for retirement.

- Since self-employed workers are not enrolled in the social security system by default, reminders and other behavioral economics tools are an alternative instrument that can help policy makers increase the coverage of the system.

- Behavioral tools could be used as policy instruments many times more cost-effective than price incentives and subsidies to increase social security contributions, even in a context of low enforceability.

- Despite being cost-effective in the short run, some behavioral interventions can have decreasing impacts after a single treatment. To affect compliance rates in the long term, policy makers should consider testing and implementing multiple treatments.