Tax Amnesties and Better Notice Letters

Context

Tax amnesties are broadly applied across countries because they generate short-term revenue gains. Many governments grant tax amnesties from time to time to collect taxes from delinquent taxpayers. A tax amnesty offers a time-limited opportunity for taxpayers to file late tax returns and regularize their outstanding tax liabilities and come into compliance. During tax amnesties, governments usually offer the enticing benefits of reduced or waived interest or penalties on late taxes.

Amnesty programs are successful in collecting taxes from noncompliant taxpayers in the short run, and tend to be particularly fruitful as complements to tougher enforcement campaigns. However, existing evidence suggests that tax amnesties fail to have long-term effects, and in some cases, generate negative effects on compliance.

The Project

To evaluate the impact of tax amnesties, this experiment considers the behavioral principle of limited attention as it looks at a redesign of the communication notices sent to taxpayers by the city of Santa Fe, Argentina. The effort aimed to reduce cognitive effort and increase understanding of the benefits of participating in tax amnesties.

In the intervention, communication notices were redesigned and sent to taxpayers to evaluate whether increasing salience (the use of color and visuals) and reducing cognitive costs (the explanation of payment plans and payment calculations) increased the probability that taxpayers paid attention to the messages and better understood the benefits of the tax amnesty. More than 54,000 taxpayers were randomized, and the intervention was conducted in May 2017. A control group of taxpayers received the regular messages that had been sent during the preceding amnesties (in September 2013 and June 2015), while a treatment group received the redesigned communications.

Behavioral Analysis

Behavioral Barriers

Limited attention: The amount of attention at our disposal at any given moment is limited, which is a reason why we tend to overlook important details and forget things. The attention of taxpayers to information received about tax amnesties could be limited by several factors, including complexities in the explanations offered.

Cognitive overload: The cognitive load is the amount of mental effort and memory used at a given moment in time. ‘Overload’ occurs when the volume of information presented exceeds an individual’s capacity to process it. Thus, the fact that our attention and memory are limited prevents us from processing all available information at the same time. Information about tax amnesties may be confusing and hard to process for individuals.

Salience: Individuals tend to focus on items or information that are more prominent and ignore those that are less so. Thus, it is important to make key aspects of messages visible and salient and display them in an appropriate place and time. A lack of color and visual information could be a significant barrier for taxpayers.

Behavioral Tools

Prominence: Human beings have limited stores of attention. Making key elements visible and prominent at the proper time and place is as important as the message itself.

Framing: The way in which information is presented influences people’s conclusions. For example, options may be presented in a way that highlights their positive or negative aspects, leading each to be perceived as relatively more or less attractive.

Simplification: Reducing the effort required to perform an action, a message could be made clearer. It could cut the number of steps involved in achieving a complex goal, or break it down into simpler steps.

Intervention Design

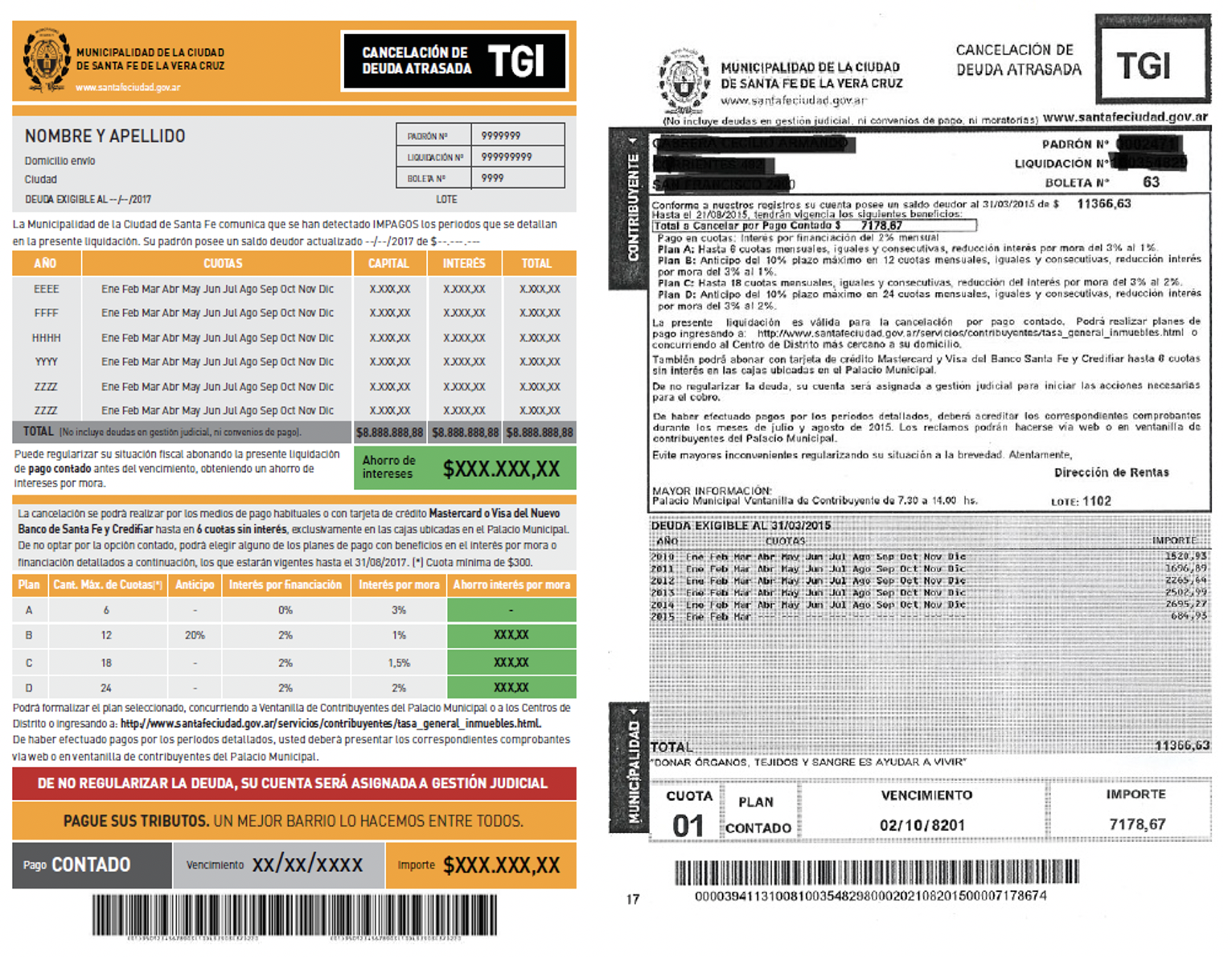

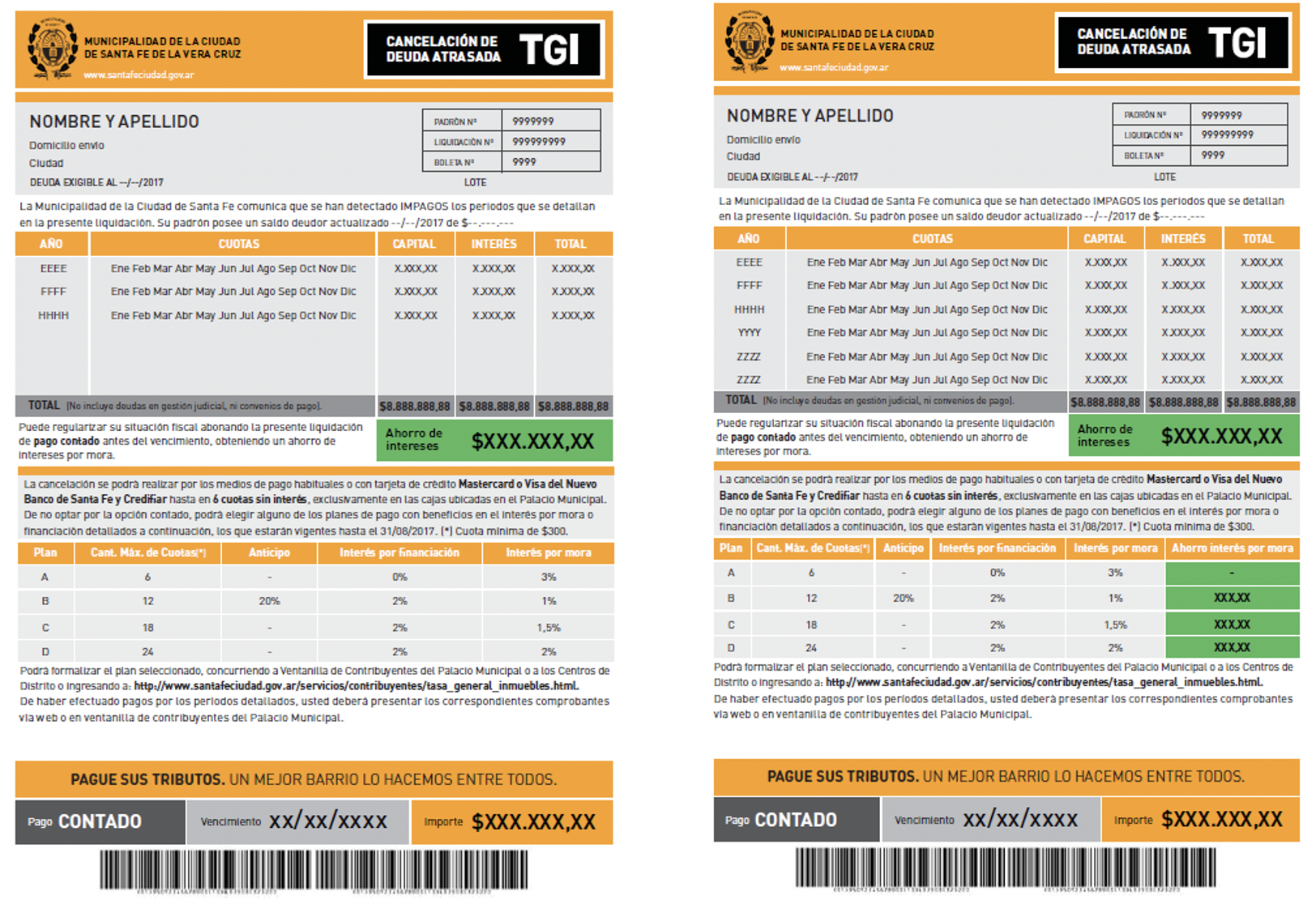

Two field experiments were run during a tax amnesty period in May 2017 in the city of Santa Fe, Argentina, with more than 54,000 taxpayers who had failed to pay their property tax bill. The first experiment included taxpayers who owed bills from January 2011 to December 2012 (about 16,000 taxpayers). The second experiment included taxpayers who accumulated debts between January 2013 and March 2017 (about 37,000 taxpayers). The age of the debt is relevant since debts become unenforceable after five years if the government fails to initiate the legal process, so authorities are likely to direct resources to older debtors and take enforcement steps absent any action.

In both experiments, standard notices mailed by the government to inform taxpayers about the tax amnesty opportunity were redesigned to show important information in a more prominent way and reduce information processing or cognitive costs. Color and other visual techniques were used, as well as an explanation of the different payment plans, including a detailed computation of the reduction in interest that each payment plan provided. The redesigned letter in the first experiment also increased the salience of a deterrence message. The second experiment included two treatment groups that received two slightly different versions of the redesigned letter, the only difference being that one version added a column with the computation of interest saved in monetary terms under each plan as opposed to showing just a percentage calculation. Control groups in both experiments received the original notices without redesign.

Figure 1. Original notice and redesigned letter, experiment 1

Figure 2. Redesigned letters A (left) and B (right), experiment 2

Challenges

Because the taxpayers involved in the study were highly heterogeneous, we divided the sample into strata according to their compliance during the period of interest (2011–17).

Results

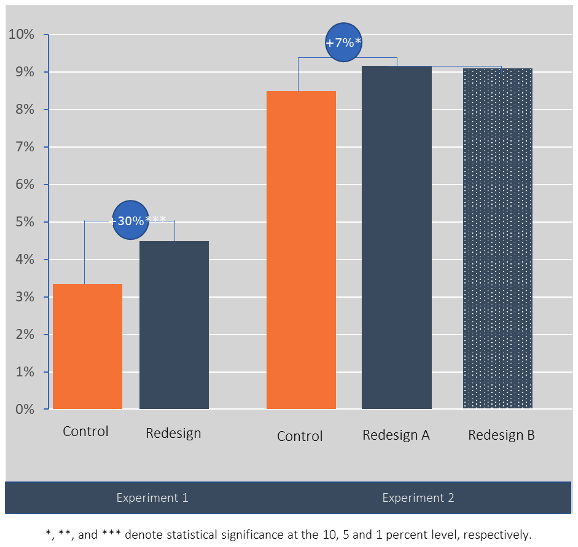

Overall results suggest that the way in which a government communicates about a tax amnesty has a significant effect. The redesigned notice was found to significantly encourage taxpayers to join the amnesty program. Among debtors reaching the five-year debt limit (first experiment), the redesign encouraged a 30 percent higher participation rate than the original notice. Among debtors with more recent debts (second experiment), receiving either version of the redesign letter led to a 7 percent higher rate of participation in the program than the original letter.

Figure 3. Probability of taxpayers joining the tax amnesty

Además, la evidencia indica que el pago promedio de los contribuyentes que recibieron las cartas rediseñadas fue significativamente más alto que el de los que recibieron la carta estándar sin modificaciones. El pago promedio fue 8% más alto comparado al grupo de control en el primer experimento y aproximadamente 6% más alto en el segundo.

Los mejores resultados en el caso de la carta rediseñada en el primer experimento comparados con el segundo son consistentes con la evidencia en la literatura sobre tributación que indica que la amenaza de actuaciones judiciales puede aumentar efectivamente el cumplimiento tributario.

Sin embargo, se observó que las amnistías fiscales tienen un efecto secundario negativo. Analizando la conducta de los vecinos de los contribuyentes que recibieron las cartas de la intervención, el estudio observa que tener información más detallada sobre la existencia de un programa de amnistía y sus beneficios en realidad puede desmotivar los pagos puntuales entre los contribuyentes que anteriormente cumplían con sus obligaciones.

Implicaciones para las políticas

- Nuestros resultados sugieren que la reducción de la carga cognitiva de los contribuyentes para procesar información puede aumentar la recaudación de los impuestos pendientes de pago, una medida que se puede emprender sin realizar grandes inversiones.

- Sin embargo, coincidiendo con la literatura no experimental, las amnistías tienen un efecto perjudicial en el cumplimiento de contribuyentes que antiguamente cumplían con sus obligaciones.

- El efecto colateral negativo de las amnistías fiscales es que puede generar incentivos negativos en el cumplimiento tributario en la población en general.

- Por lo tanto, las amnistías fiscales deberían utilizarse moderadamente, en el contexto de reformas fundamentales que presentan una lógica clara que justifique una amnistía, y sólo si la amenaza de una mayor vigilancia del cumplimiento es real y es utilizada por gobiernos que pueden asegurar que respetan los compromisos intertemporales.