Testing Fiscal Exchange Appeals

Context

Tax noncompliance hinders the financing of public services for citizens. Enforcement, a crucial tool for any tax administration, has its limits (e.g., technical, legal, moral, and political). In the present context of a severe economic crisis in Argentina, the local government made a priority of persuading taxpayers to comply voluntarily. This decision coincides with a growing interest in explaining what motivates individuals to pay their taxes, and how cost-effective complements to enforcement actions can create a culture of compliance. The starting point of the project was that tax bills lacked a persuasive and salient explanation of why and how to pay taxes. If mere wording differences in the presentation of the tax bill can increase tax revenues during an economic crisis, then tax authorities might be able to increase revenues through the provision of better public services and improved communication.

The Project

The project aimed at providing the Municipality of Mendoza with tools and a methodology to test and implement administrative changes to improve tax compliance. The Municipality and the IDB team redesigned the tax bills for the local property tax (tasas). In line with the municipality’s making amicable interventions a priority, the redesign centered on simplifying information and appealing to the fiscal exchange inherent in taxation—i.e., making salient that with tax monies, the administration can provide taxpayers with valued public services. The experimental treatments (tax bills) were delivered in November 2019.

Behavioral Analysis

Behavioral Barriers

Limited attention: The amount of attention at our disposal at any given moment is limited, which is a reason why we tend to overlook important details and forget things. In this context, taxpayers who in principle are willing to consider the social benefits of taxation in their tax compliance decision, may fail to do so under standard circumstances—i.e. without an explicit reminder of these benefits.

Mistrust: Mistrust occurs when one party is unwilling to rely on the actions of another party in a future situation. Taxpayers who do not trust a government administration may use this as a justification for tax evasion.

Present bias: It is the tendency to choose a smaller gain in the present over a large gain in the future. It is related to the preference for immediate gratification. It is also known as hyperbolic discounting. People with such a bias might value present gratification more than greater benefits in the future—for example, they might avoid paying taxes even when there is a possibility of winning a lottery.

Behavioral Tools

Signaling: The act of conveying credible information to others about one’s expected actions or behavior.

Moral suasion: The act of persuading a person or group to act in a certain way through theoretical appeals, persuasion, or implicit and explicit threats. In the present context, a visually supported appeal to the “fiscal exchange” of taxes for services aims at persuading taxpayers of their self-interest. This message might be associated with positive emotions, for example, by advertising public services that benefit children (e.g., renovated playgrounds) with visuals.

Intervention Design

The project tested three different municipal property tax bills (treatments). At the municipality’s request, we randomized the treatments to small geographical zones. For a clean analysis, we considered 22,119 taxpayers in 1,593 zones that had not also participated in another intervention. Municipal agents delivered the tax bills November 4–11, 2019, and recorded in-person deliveries, if possible. The bills featured two due amounts (November 21 and December 19, 2019). The data we analyze includes payments through January 9, 2020.

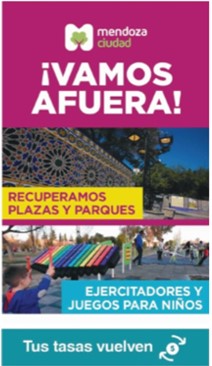

Figure 1. Public Service Advertisement (Key Element of Treatment T3)

The three treatments tested include the existing bill (T1), a redesigned bill without public service advertisement (T2), and a redesigned bill with public service advertisement (T3). The key element of fiscal exchange (T3) is shown in figure 1. For taxpayers in arrears, there was language urging the payment of outstanding taxes and avoiding judicial proceedings. This language was identical, but possibly more salient, in the new tax bills.

The theory of change posits that the new, simplified bills, in color, will (1) capture the taxpayer’s attention, (2) signal that the tax administration is giving renewed attention to the collection of this tax, (3) indicate more saliently where to pay, and (4) enhance the taxpayer’s perception of a fiscal contract in which valued public services are provided in return for tax payments. Each of 1–4 might lead to increased compliance. The comparison of T2 and T3 isolates the fiscal-exchange appeal effect (4). T1 provides a benchmark for the overall effects of the changes.

Challenges

To alleviate potential confusion among neighbors receiving different-looking tax bills and to facilitate logistics, treatments were randomized to small geographical zones. To avoid contamination from another innovation, tax debtors affected were excluded from the analysis. Printing in color represented an additional cost compared with costs of the standard black-and-white tax bills.

Results

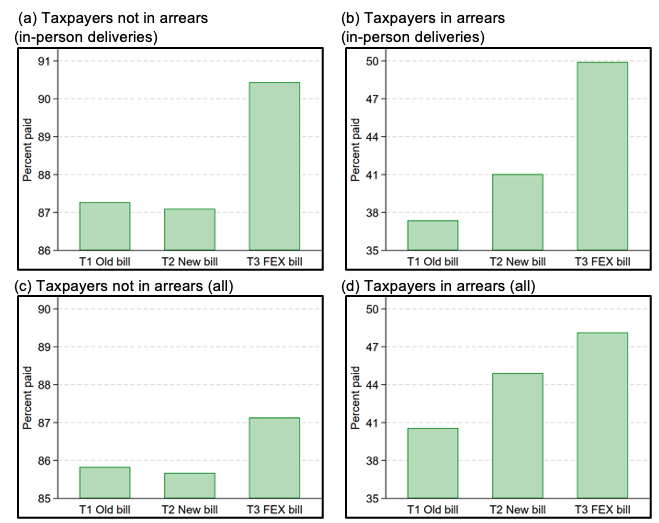

Figure 2 presents an overview of results, plotting the percentage of taxpayers in each treatment group who made a payment for the Nov.–Dec. municipal property tax bill.

Figure 2. Treatment Effects as a Proportion of Paying Tax Bill

Notes: T1 represents the control group (old bill design), T2 the redesigned tax bill, and T3 is the redesigned tax bill that has a public services advertisement (“FEX” stands for fiscal exchange).

- For taxpayers not in arrears, the fiscal exchange bill increased payment rates from about 87 percent to more than 90 percent if the bill was delivered in person (see figure 2a, above).

- For taxpayers in arrears, payment rates increased from 38 percent with the old design to 50 percent with the fiscal exchange appeal if the bill was delivered in person (figure 2b). The payment rate for the new design without the fiscal exchange appeal was 41 percent in this group.

- Among all taxpayers, i.e., without conditioning on in-person delivery, the treatment differences are qualitatively similar, albeit somewhat smaller.

- In addition to the effects on paying the tax bill, the new bills (T2 and T3) increased the share of tax delinquents who paid arrears from about 17 percent to about 22 percent.

Policy Implications

- Given the unfavorable context of an economic crisis and mixed prior findings in the literature, the small communications changes had surprisingly positive effects on noncompliant taxpayers. This suggests similar interventions might increase tax compliance in a larger range of circumstances than previously thought. Practitioners should consider that effects likely diminish over time.

- The fiscal exchange appeal had a strong visual element that highlights how public services benefit children, two nonstandard elements that may have contributed to the positive effect. Furthermore, the municipal setting may have helped because taxpayers may have seen and used exactly the goods advertised. Policy makers may want to cater message content and delivery in ways that work for local context.