The Role of Credit and Credibility in Tax Compliance

Context

Tax noncompliance hinders the financing of public services for citizens. Amid a national economic crisis, an Argentinian municipality of 40,000 inhabitants tested two approaches to address nonpayment by local business taxpayers: (i) sending a redesigned tax dunning letter, inspired by the behavioral literature, and (ii) adding a novel deterrence element: informing businesses that continued nonpayment might reduce their access to credit, as the municipality would forward nonpayment information to a major credit rating bureau.

The Project

The project aimed at evaluating changes in collecting local business tax arrears implemented by an Argentinian municipality in the northwestern province of Corrientes in 2019. To this end, the IDB collaborated with the municipality’s public finances team. The IDB team randomized the three different tax dunning letters, which were delivered by municipal agents to the businesses in arrears (in June and again in September). Thereafter, the municipality informed the credit bureau about the delinquency status of 50 business taxpayers. After the intervention, between October and December, the local team conducted a post-intervention survey.

Behavioral Analysis

Behavioral Barriers

Limited attention: People’s ability to process information is limited. As a result, they tend to overlook important details and forget things. The attention of the taxpayers to the information received about tax amnesties could be limited due to several factors including complexities in the explanation about the process to follow.

Present bias: It is the tendency to choose a smaller gain in the present over a large gain in the future. It is related to the preference for immediate gratification. It is also known as hyperbolic discounting. People with such a bias might value present gratification more than greater benefits in the future—for example, they might avoid paying taxes even when there is a possibility of winning a lottery.

Salience: Individuals tend to focus on items or information that are more prominent and ignore those that are less so. Thus, it is important to make key aspects of messages visible and salient and display them in an appropriate place and time. The lack of color and visual information could be an important barrier for the taxpayers.

Other Barriers

Mistrust: Mistrust occurs when one party is unwilling to rely on the actions of another party in a future situation. Taxpayers who do not trust a government administration may use this as a justification for tax evasion.

Behavioral Tools

Signaling: The act of conveying credible information to others about one’s expected actions or behavior.

Moral suasion: This is the act of persuading a person or group to act in a certain way through theoretical appeals, persuasion, or implicit and explicit threats. Here, the new tax dunning letters provided examples of public investments financed with tax revenues.

Planning tools: These are designed to encourage individuals to make a concrete action plan on important goals, like paying their taxes. These prompts help individuals to break down a goal (e.g., being on time to a doctor’s appointment) into a series of small, specific tasks (e.g., leaving work early, finding a babysitter, postponing a weekly meeting, etc.) and to anticipate unforeseen events. These prompts often encourage people to write down relevant information such as instructions on ways to make an appointment with the tax administration were included.

Intervention Design

The project tested three different dunning letters regarding municipal tax payment (treatments): the existing dunning letter (T1), a redesigned letter inspired by the behavioral literature (T2), and a version of T2 with an additional element, deterrence, whereby tax delinquents were told that their nonpayments might be reported to a credit bureau, limiting their access to credit (T3).

We randomized treatments to business taxpayers within five strata defined by combinations of debt amount plus recent payment activity. In addition, a separate stratum was established for families that owned multiple businesses; the same letter design was delivered to family members to minimize treatment contamination. The sample consisted of 1,238 business tax delinquents. About half of them were no longer active, confirming how badly outdated the local tax registry was.

Because of systematic differences in the delivery dates of the old vs. new letters, we focus on comparing the two new redesigns. The unique difference between T2 and T3 (the deterrence element shown in figure 1, below) facilitates interpretation, unlike the case of the multiple differences between the old and new designs. The theory of change here is that the threat of losing access to credit prompts some businesses to repay part of their tax debt.

Figure 1. Deterrence: How T3 Differs from T2

Notes: This part of the T3 tax dunning letter announced that local tax authorities would inform a major credit bureau about delinquent taxpayers, potentially threatening their access to credit.

Challenges

- The population under study comprised local taxpayers with the most extensive history of arrears, and assumed as least likely to make payments in response to an intervention.

- The tax registry was outdated. About half the sample was inactive ex-post, reducing the already limited statistical power.

- Systematic differences in the delivery dates of old vs. new letters undermined identification of treatment effects with respect to the status quo (T1).

- As in many surveys, only a fraction participated (in this one, a third of the sample).

Results

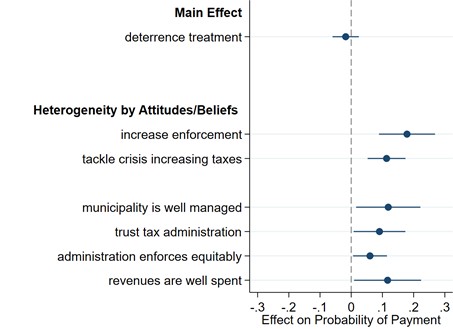

Figure 2 presents an overview of preliminary results. It compares the effects of T2 (new design) vs. T3 (new design plus deterrence [threat] language) on outcome (did recipients make a debt repayment within 60 days of receipt).

The top element in figure 2 (“main effect”), indicates that tax-debt repayments are not significantly more or less likely in T2 vs. T3. Was this because taxpayers did not care about the credit rating threatened in T3? Or because they doubted the local authorities would follow through? The survey data provides insights: Although a majority classify the credit rating as at least somewhat important, most believe that tax noncompliance has no consequences whatsoever. These assessments do not significantly differ between T2 and T3. Also, across all treatments, about 90 percent indicate that many, if not most, taxpayers are waiting for an amnesty that would regularize their tax debt. Only 10 percent of taxpayers in T3 think that the municipality reports tax delinquents to a credit bureau. In other words, the credibility around the municipality’s enforcement ability seems low.

Figure 2. Main and Heterogeneous Effects of Deterrence (T3)

The heterogenous effects of T3 regarding attitudes and beliefs are suggestive. For those taxpayers expressing a preference for stronger enforcement or increasing taxes to tackle revenue shortcomings during crisis, the deterrence treatment had significantly more positive effects on payment. The same holds for taxpayers with a positive assessment of municipal management, of how revenues are spent, and with trust in the local tax authorities. These heterogeneities suggest those more supportive of enforcement, and with a more positive view of the administration, were more likely to repay debt in response to the deterrence message, despite low overall credibility.

Policy Implications

- Despite the lack of an overall effect of the threat of informing a credit bureau about delinquency status and low credibility, taxpayers with a more positive opinion of the local administration and more supportive of enforcement appear more inclined to make a debt payment in response. However, most taxpayers, it seemed, preferred waiting for an amnesty to regularize their debt.

- The results suggest, first, that the effectiveness of enforcement actions hinges on their credibility; second, that a positive assessment of government performance and enforcement may be complements in prompting compliance; and, third, improving tax administrative fundamentals such as the tax registry may be a priority.

Annex. Survey

The survey variables are as follows (translated from Spanish), integer scales from 1 to 5:

Increase enforcement

In your opinion, should the intensity of municipal tax enforcement:

1=decrease a lot, 2=…, 3=…, 4=…, 5=increase a lot

Tackle crisis, increase taxes

To address reduced revenues during a crisis like this, should municipal governments increase tax rates? Order this and other alternatives [omitted]:

1=least preferred, …, 5=most preferred

Municipality well managed

How do you evaluate the management of the municipality overall?

1=do not approve at all, …, 5=approve strongly

Trust tax administration

To what extent to you trust the tax administration of [name of municipality]?

1=not at all, …, 5=a lot.

Administration enforces equitably

To what extent do you agree with the following statement? The local tax administration makes everybody comply with the tax obligations equally.

1=disagree completely, …, 5=agree completely

Revenues well spent

Please indicate your opinion about the use of local tax revenues:

1=very badly used, …, 5 =very well used